For last week, the S&P 500 ($SPX) finished up 1.22%, the Nasdaq ($QQQ) closed out the week at a new high with its 2.63% gain, and Small Caps ($IWM) closed on Friday just under their 20-week Moving Average and up 1%. This week’s Technical Market Outlook focuses on commodities and Treasury’s as well as the typical charts I show each week.

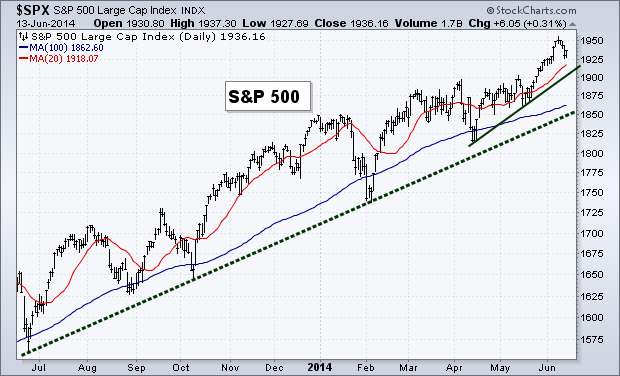

Trend

While we had that short-lived sell-off, the S&P 500 found support at its 100-day Moving Average and didn’t get the chance to even touch its trend line off the prior lows. The index is now back above both its short- and long-term Moving Averages as trend remains in favor of the bulls. I tweeted out on Friday the levels of resistance I’m watching, we were unable to close above either of them on Friday so I’ll continue to keep an eye here this week.

Breadth

As we started into August I noted that there had been a small negative divergence that was created in the Advance-Decline Line. While these types of occurrences typically lead to lower prices, it wasn’t big enough to cause us to worry of a protracted decline. The drop two weeks ago took the A-D Line back to its trend line where it found support.

Commodities

In my Where Are We In The Business Cycle? post back in December of last year, I showed the stock, bond, and commodity markets as I discussed some of the work done by John Murphy. While there are many different indices and ETFs that track the commodity market the GSCI Index is one of the broadest with a fairly long track record. However, I will say it gives a large weighting to crude oil. Earlier this year we saw $GSG run into its previous high which sent price falling and it has now broken through its bull market trend line.

This doesn’t mean that commodities are no longer in a bull market, but this is a fairly significant break and I’m watching to see how long it spends under the support line and if it now becomes resistance on any future advances. Commodities started out the year with a big move higher, but the last couple of months have not been kind. As we start to finish up the bearish period of seasonality, will commodities be able to rebound?

Commodities vs. Treasury’s

Commodities vs. Treasury’s

Sticking with the topic of commodities I want to show this next chart that has the ratio between The 10-Year Treasury and the CRB Commodity Index. You’ll notice this chart looks almost like a mirror image of the $GSG chart above. As Treasury’s rally the ratio between the 10-Year and commodities is close to breaking resistance. I’m curious if this will slow down the Treasury rally and if we see things cool off or if this ratio continues to march higher to the previous high in 2013.

Momentum

Momentum

Like breadth, we saw momentum test support after the 4% drop in stocks. The Relative Strength Index fell back and tested previous support before bouncing and heading higher. After also diverging, the MACD has now seen a crossover of its fast and slow lines as stock prices attempt to rally back.

Bond Market

Bond Market

The theme so far for 2014 has been bond divergence. The chart below shows the ratio between High Yield and Treasury bonds and then the 10-year Treasury yield along with the S&P 500. We haven’t seen this large of a divergence between these two bond measurements since prior to the 2011 correction.

In my opinion there’s one of two things that is happening right now as it pertains to stocks and bonds:

1. The bond is trying to signal that something isn’t right. While stocks have been taking out new highs, High Yield bonds ($HYG) have been taken to the woodshed relative to their perceived saver brethren, Treasury’s. During the current bull market when High Yield bonds and Treasury yield have headed to the exits in the face of an advancing stock market, it was the fixed income market that got things right. Is it different this time?

Or 2. The correlation between bonds and stocks is changing. The 30-week correlation between the S&P 500 ($SPX) and the 10-Year Yield ($TNX) is at the lowest level since 2006. While typically we seen bonds and stocks trade inverse from one another, historically that hasn’t always been the case. During much of the 90’s we saw interest rates fall while stocks headed higher.

Of course there could be a third option, that the bond market has things wrong and will correct as stocks stabilize and keep the up trend in tact. Luckily the “why” isn’t all that important for those that rely on price action to dictate their bias. However, what’s happening in the fixed income market is interesting and if you believe it’s sending a warning signal for stocks, then the chart below is pretty tough to ignore.

60-Minute S&P 500

60-Minute S&P 500

While there was a negative divergence in momentum going into the 4% sell-off, we also saw a positive divergence to help signal the ‘all clear.’ While price made lower lows on this intraday chart, the Relative Strength Index and MACD indicators began to rise, creating a bullish divergence. Price eventually confirmed and broke back over its 50 one hour Moving Average.

Last Week’s Sector Performance

Last Week’s Sector Performance

Last week Health Care ($XLV) was the best performing sector followed by Tech ($XLK) and Consumer Staples ($XLP). While Energy ($XLE), Financials ($XLF) and Materials ($XLB) were the worst performing sectors for the week.

Year-to-Date Sector Performance

With the energy sector’s weakness over the last couple of weeks it has lost its place as one of the top two sectors for 2014. Health Care has moved into the top spot, followed by Utilities ($XLU) and Technology. Consumer Discretionary ($XLY), Industrials ($XLI) and Financials remain the worst performers for the year.

Disclaimer: Do not construe anything written in this post or this blog in its entirety as a recommendation, research, or an offer to buy or sell any securities. Everything in this post is meant for educational and entertainment purposes only. I or my affiliates may hold positions in securities mentioned in the blog. Please see my Disclosure page for full disclaimer. Connect with Andrew on Google+, Twitter, and StockTwits.